The Myth: "SIP Is Always Better"

Vikram received ₹20 lakh as a bonus in March 2020 — right at the bottom of the COVID market crash. His advisor told him to spread it via SIP over 12 months. By September 2020, the Nifty 50 had recovered almost entirely. Vikram's SIP missed much of the recovery — his first instalment earned the most, and his later instalments bought units at much higher prices. A lumpsum at the March bottom would have significantly outperformed.

The reverse scenario is equally true. Investors who dumped lumpsum into equity in January 2008 watched it fall 60% over the next 14 months. A 12-month SIP starting that same day would have averaged down beautifully and recovered much faster.

The honest reality: neither SIP nor lumpsum is always better. The right answer depends on market conditions, the amount available, and your psychological capacity to handle volatility.

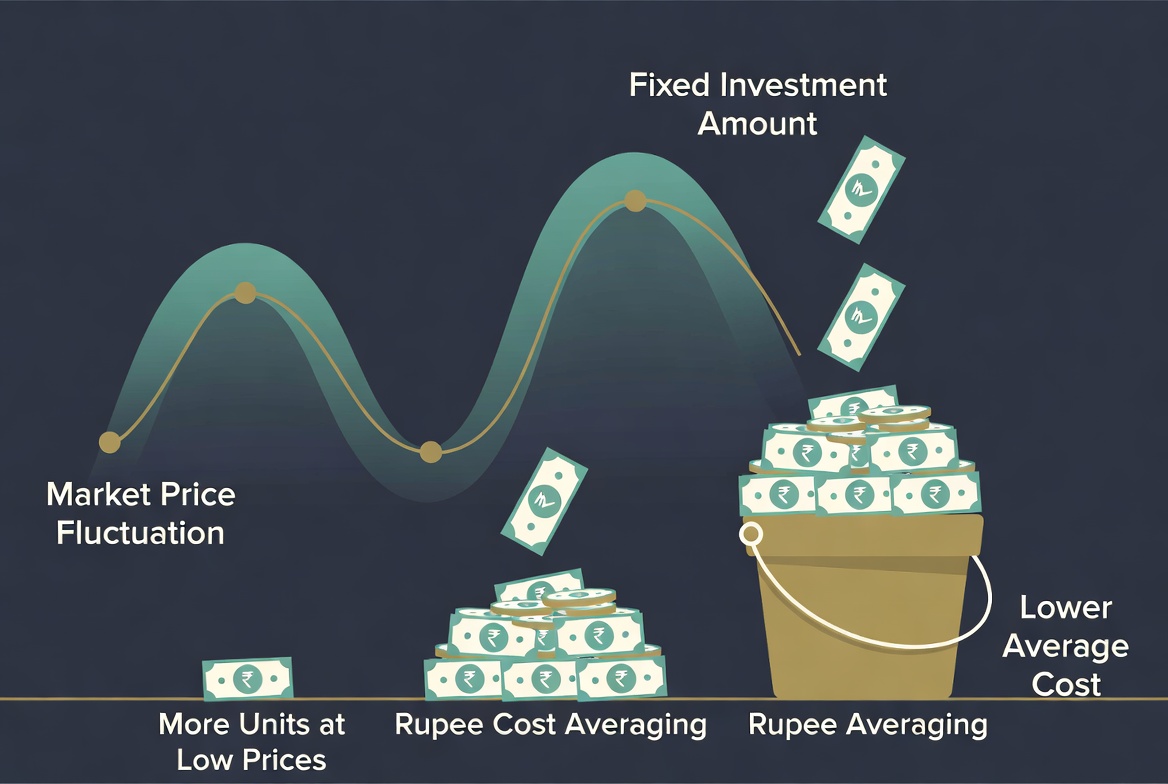

How Each Method Actually Works

Real Scenarios: When Each Method Won

| Market Scenario | Market Behaviour | SIP Result | Lumpsum Result | Winner |

|---|---|---|---|---|

| COVID Crash & Recovery (Mar 2020) | Sharp 38% fall, V-shaped 8-month recovery | Averaged down, strong recovery | If invested at bottom: outstanding | Lumpsum (if timed right) |

| 2008 Global Financial Crisis | 60% crash over 14 months, slow recovery | Averaged down, recovered sooner | Down 60%, slow recovery | SIP |

| 2017–2018 Bull Run | Steady upward trend, 28% Nifty return in 2017 | Later instalments bought at higher NAV | Full corpus benefited from Day 1 | Lumpsum |

| 2011 Sideways Market | Market flat ±10% throughout the year | Cost averaging, no impact difference | No gain for sitting idle in equity | Draw / SIP slight edge |

| 2020–2023 Post-COVID Bull Run | Sustained 3-year rally, Nifty 2x | Solid returns, each instalment up | Exceptional if entered in 2020 | Lumpsum (timing critical) |

| Typical 10-Year Average | Mix of ups, downs, recovery cycles | 12–13% CAGR historically | 12–13% CAGR (similar, random entry) | Statistical Tie |

The Middle Path: STP (Systematic Transfer Plan)

What if you have a large lumpsum — say ₹10 lakh — but don't want to time the market? The Systematic Transfer Plan (STP) gives you the best of both worlds.

💡 Use the Lumpsum calculator to see how ₹5L invested today compares to ₹10k/month SIP over 10 years.

Try the calculator → 💬 Get a personalised planSTP is particularly powerful for bonus recipients, retirees with a corpus to deploy, or anyone receiving a large inheritance. The liquid fund earns you a return while your equity entry is staggered — you are never "out of the market" entirely.

Interactive Lumpsum vs SIP Comparison Calculator

Which Would Have Done Better for You?

Tax Reality: What Changes Between SIP and Lumpsum

Who Should Choose What?

- Salaried investor with monthly income: SIP — non-negotiable. It aligns investing with your income rhythm, removes timing decisions, and automates wealth building.

- Bonus recipient (₹2L–₹20L): STP — park in a liquid fund, set a 6–12 month STP into equity. Best of both worlds.

- Market crash investor (Nifty down 25%+): Lumpsum with conviction. This is the rare scenario where timing is clear enough to justify lumpsum entry.

- Retiree deploying PF corpus: STP over 18–24 months — never lumpsum into equity. Use debt funds as the parking vehicle.

- Long-term investor indifferent to timing: Either works over 15+ years. Mathematical difference narrows significantly over very long horizons.

FAQs

Expert Verdict

The SIP vs lumpsum debate has a simple answer and a nuanced one. The simple answer: if you have a monthly income and are building long-term wealth, SIP wins — not because it always generates higher returns, but because it works for virtually every market condition, removes the dangerous trap of market timing, and aligns with how most Indian investors actually receive money. The nuanced answer: if you receive a large lumpsum and have the wisdom to recognise a genuine market correction, a lumpsum or STP approach at that specific moment can meaningfully outperform a staggered SIP.

The most important reality check in this entire debate is behavioural: lumpsum investing in the hands of the average retail investor tends to happen at market peaks — when confidence is highest and valuations most stretched. SIP investing, by design, prevents this. Which is why, for the vast majority of the investors we serve at Sampatha Setu, SIP remains the single most reliable wealth-building tool available — not because the mathematics always favour it, but because human psychology almost always works against the alternatives.

SIP, Lumpsum, or STP — Get the Right Call for Your Situation

Our advisors will evaluate your income pattern, corpus size, and market context to recommend the optimal investment approach for your specific situation.

💬 Book a Free Strategy SessionRead next: Bamboo Tree Investing — the art of patient wealth creation · Power of Compounding — why time beats everything